Stop Building Fintech Analytics In-House: A $350K Mistake

Here’s a number that should make every fintech CTO pause: 81% of fintech companies now embed analytics into their products. That’s not a future trend. That’s the baseline expectation in 2026.

But here’s the part that doesn’t show up in the trend reports: most of those companies burned six figures trying to build analytics in-house before realizing they’d made a very expensive mistake.

The reasoning always sounds solid at the start. “We’re an engineering-driven company. We build things. How hard can dashboards be?” Turns out, very hard — especially when your engineering team is already stretched across compliance deadlines, real-time payment rails, fraud detection pipelines, and the AI features your board saw a competitor ship last quarter.

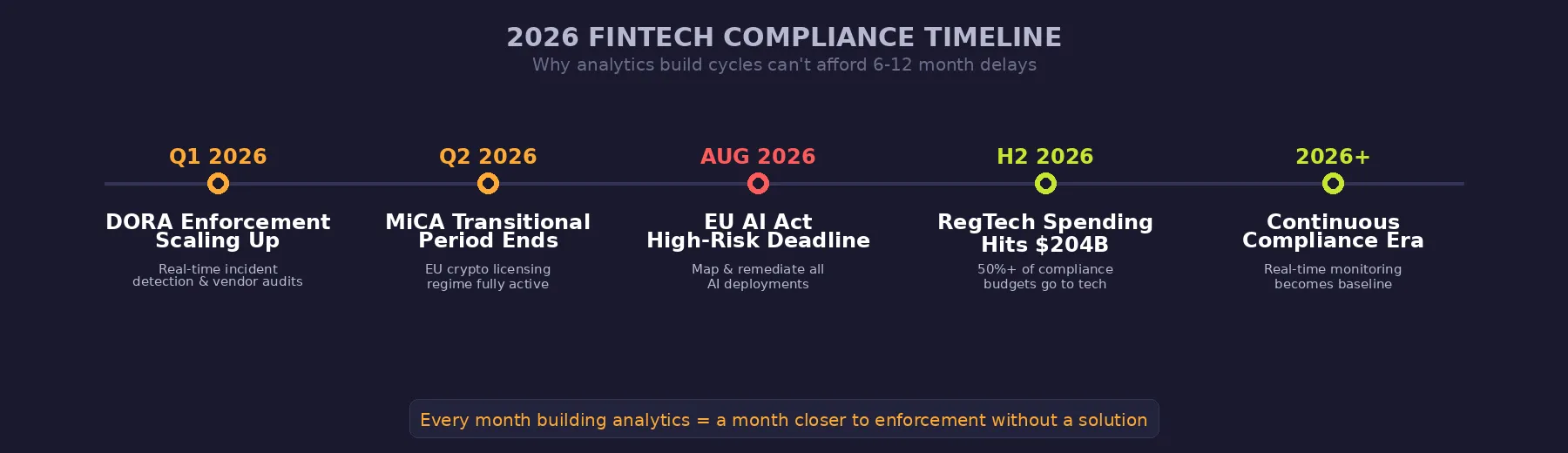

The fintech landscape in 2026 isn’t forgiving. The EU AI Act’s high-risk obligations kick in this August. DORA enforcement is scaling. MiCA’s transitional period ends mid-year. RegTech spending is projected to hit $204 billion. And AI-powered analytics — natural language queries, autonomous data agents, predictive dashboards — aren’t premium features anymore. They’re what your customers expect to see when they log in.

This article breaks down the real cost of building fintech analytics in-house versus buying an embedded analytics platform, with data, timelines, and a decision framework specific to financial technology in 2026.

The $350K+ Line Item Nobody Budgeted For

Let’s start with the number everyone underestimates: the actual cost of building analytics in-house.

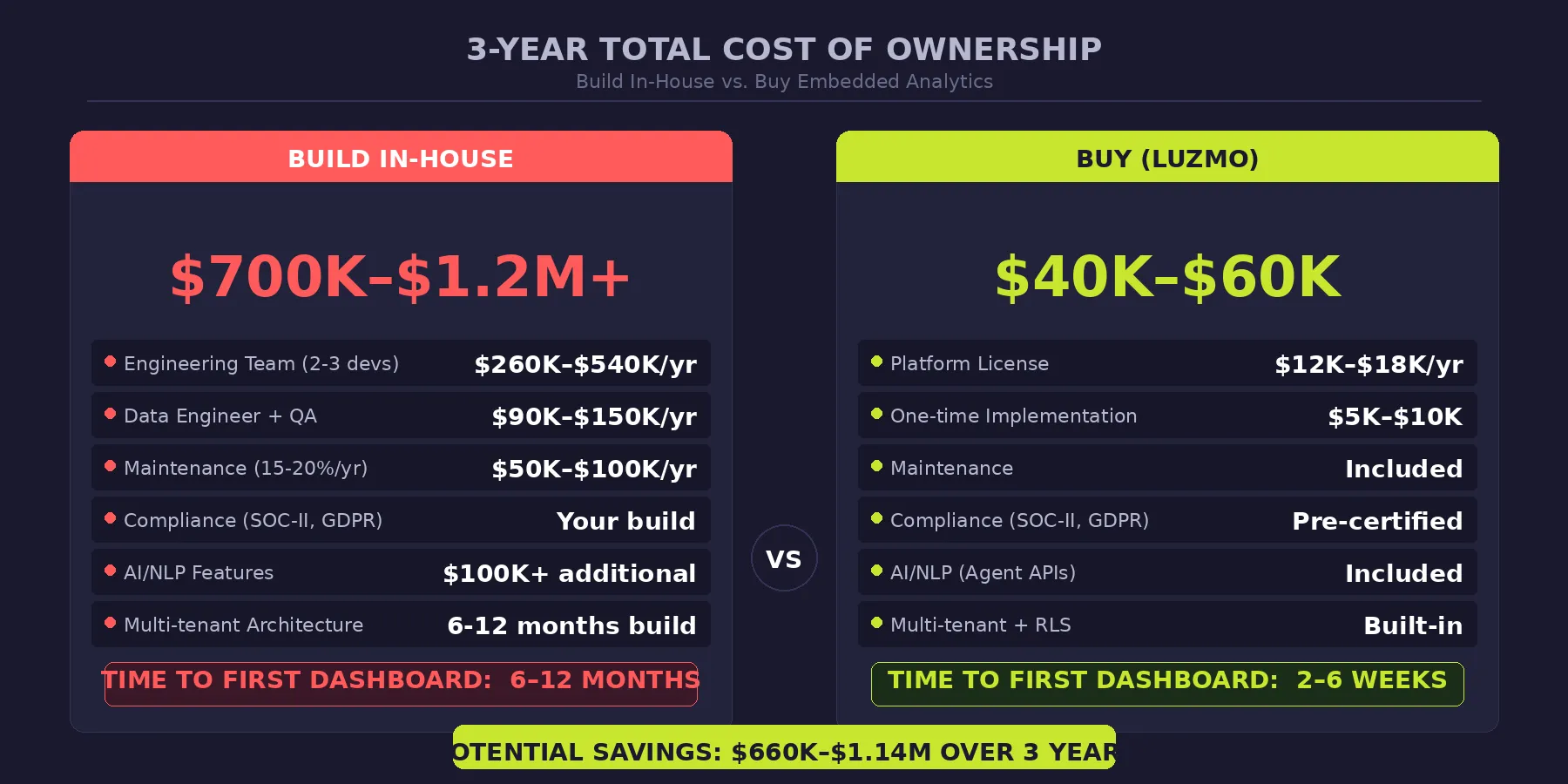

A minimum viable analytics build for a fintech product requires at least two to three full-stack developers with data visualization experience. In 2026, fintech developers in the US command an average salary of around $129,000 per year, with senior engineers specializing in AI or data reaching $180,000 or more. That’s $260K–$540K in engineering salaries alone — before you add a data engineer, a QA specialist, or the infrastructure costs.

But the initial build is just the beginning. Industry benchmarks consistently show that analytics maintenance runs 15–20% of the original build cost annually. That’s another $50K–$100K per year in bug fixes, performance optimization, new chart types, and keeping up with data source changes. Over three years, you’re looking at $700K to $1.2 million in total cost of ownership.

Now add the fintech-specific complexity that generic build-vs-buy articles don’t mention:

- Multi-tenant architecture with data isolation — mandatory when different financial institutions or end-users share your platform. Building proper row-level security from scratch is a months-long engineering project.

- Compliance certification — SOC-II, GDPR, and increasingly DORA and EU AI Act requirements. Each certification cycle costs time and money, and your homegrown analytics layer needs to pass the same audits as your core product.

- AI and natural language features — your competitors are shipping conversational analytics, auto-generated insights, and AI-powered anomaly detection. Building these from scratch requires ML engineering expertise on top of your existing team.

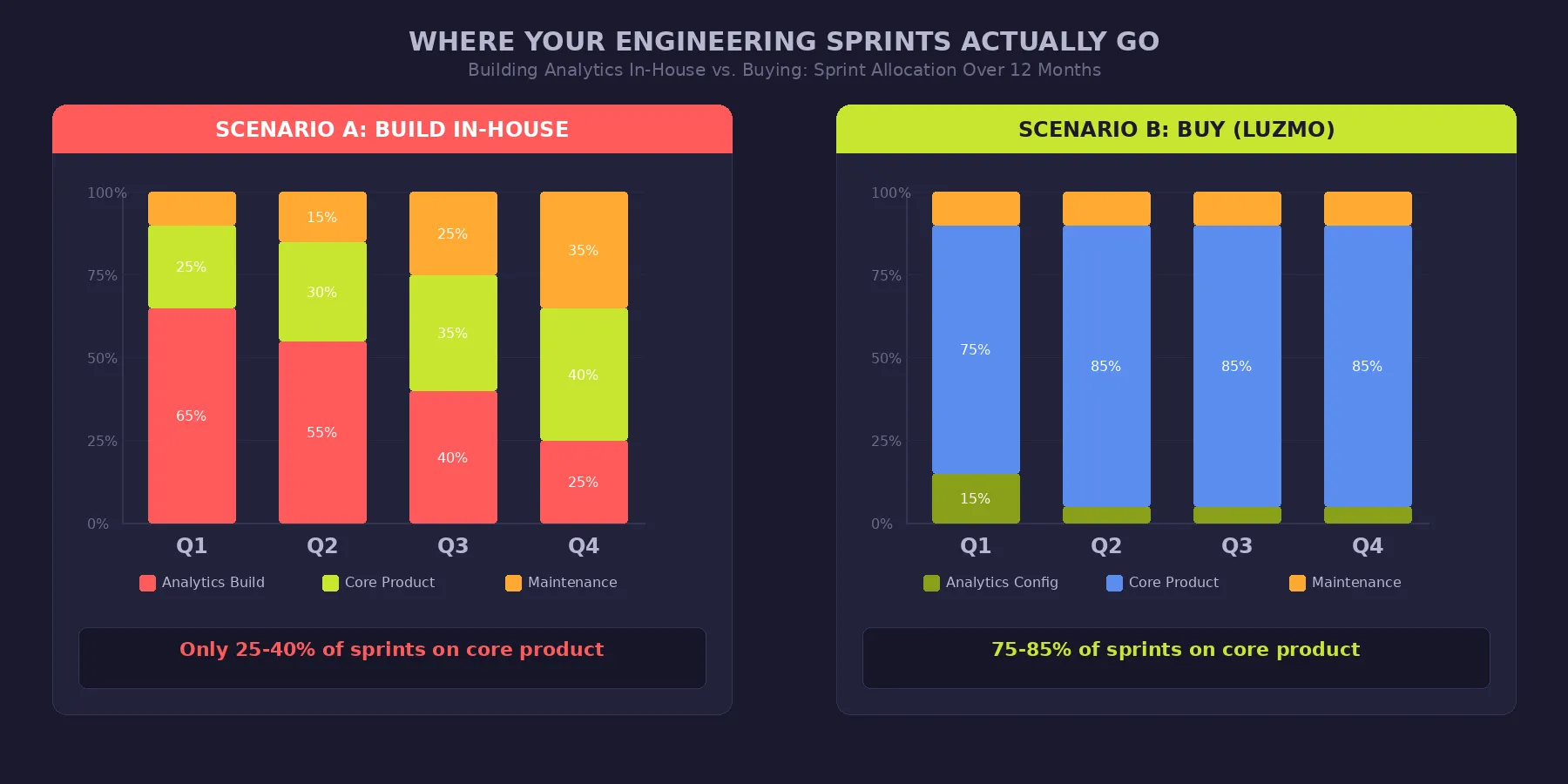

And then there’s the cost nobody puts in a spreadsheet: opportunity cost.

Every sprint your engineering team spends building chart components is a sprint they’re not spending on the features that actually differentiate your fintech product — the lending algorithms, the payment orchestration, the fraud models.

Sources: ZipRecruiter fintech developer salary data ($129K avg), Georgia Fintech Academy 2025 salary guide ($95K–$180K range), DataM Intelligence (compliance costs = 10–15% of bank revenue), Luzmo pricing.

Where Fintechs Actually Need Embedded Analytics

The build-vs-buy decision hits differently depending on what you’re building analytics for. Here’s how it plays out across the fintech use cases that matter most in 2026.

Real-Time Fraud & Risk Analytics

AI-powered fraud detection has already reduced industry losses by an estimated 40%, according to recent market analysis. But fraud teams in 2026 don’t just need static dashboards showing yesterday’s alerts. They need autonomous agents that triage incidents, flag anomalies in real-time, and escalate only the complex cases to humans.

Building this from scratch means engineering real-time data pipelines, anomaly detection models, alerting systems, and interactive visualizations — on top of the compliance requirements that govern how financial transaction data can be displayed and stored. An embedded analytics platform with AI capabilities (like Luzmo’s Agent APIs) delivers natural language queries on transaction data, auto-generated summaries, and intelligent alerts out of the box.

Personalized Lending & Credit Decisioning

Roughly 60% of digital lending now relies on AI for credit decisions, with borrowers increasingly expecting transparent, real-time visibility into their application status and portfolio performance. For lending platforms, analytics isn’t a nice-to-have — it’s the interface through which borrowers and lenders interact with their money.

The challenge is multi-tenancy. Each lender, borrower, and institutional partner needs to see only their data, with their branding, in their timezone and currency. Building this kind of role-based, white-labeled analytics experience in-house is one of the most underestimated engineering projects in fintech. Platforms like Luzmo handle multi-tenant architecture, row-level security, and white-label branding natively — what would take months to build ships in weeks.

RegTech & Compliance Reporting

RegTech spending is projected to reach $204 billion by 2026, according to Juniper Research, with regulatory technology accounting for more than half of all compliance budgets globally. That’s not a niche — that’s the new operating reality.

For fintechs navigating DORA, the EU AI Act, and evolving AML/KYC requirements, compliance analytics means real-time monitoring, audit-ready dashboards, and automated reporting. Building all of this in-house means your analytics project inherits the full weight of your compliance obligations. Buying from a vendor that’s already SOC-II and GDPR certified eliminates months of audit preparation and shifts compliance liability off your engineering roadmap.

Payments & Transaction Analytics

The numbers here are staggering: instant payment value is expected to grow from $22 trillion in 2024 to nearly $58 trillion by 2028. Payment platforms processing these volumes need sub-second analytics on transaction flows, settlement timelines, and reconciliation status.

This is where query engine performance matters. Slow-loading dashboards in a payments context don’t just annoy users — they cost money. Luzmo’s Warp query engine and native multi-currency/multi-timezone support address exactly this: lightning-fast dashboards that work across global financial operations without custom engineering.

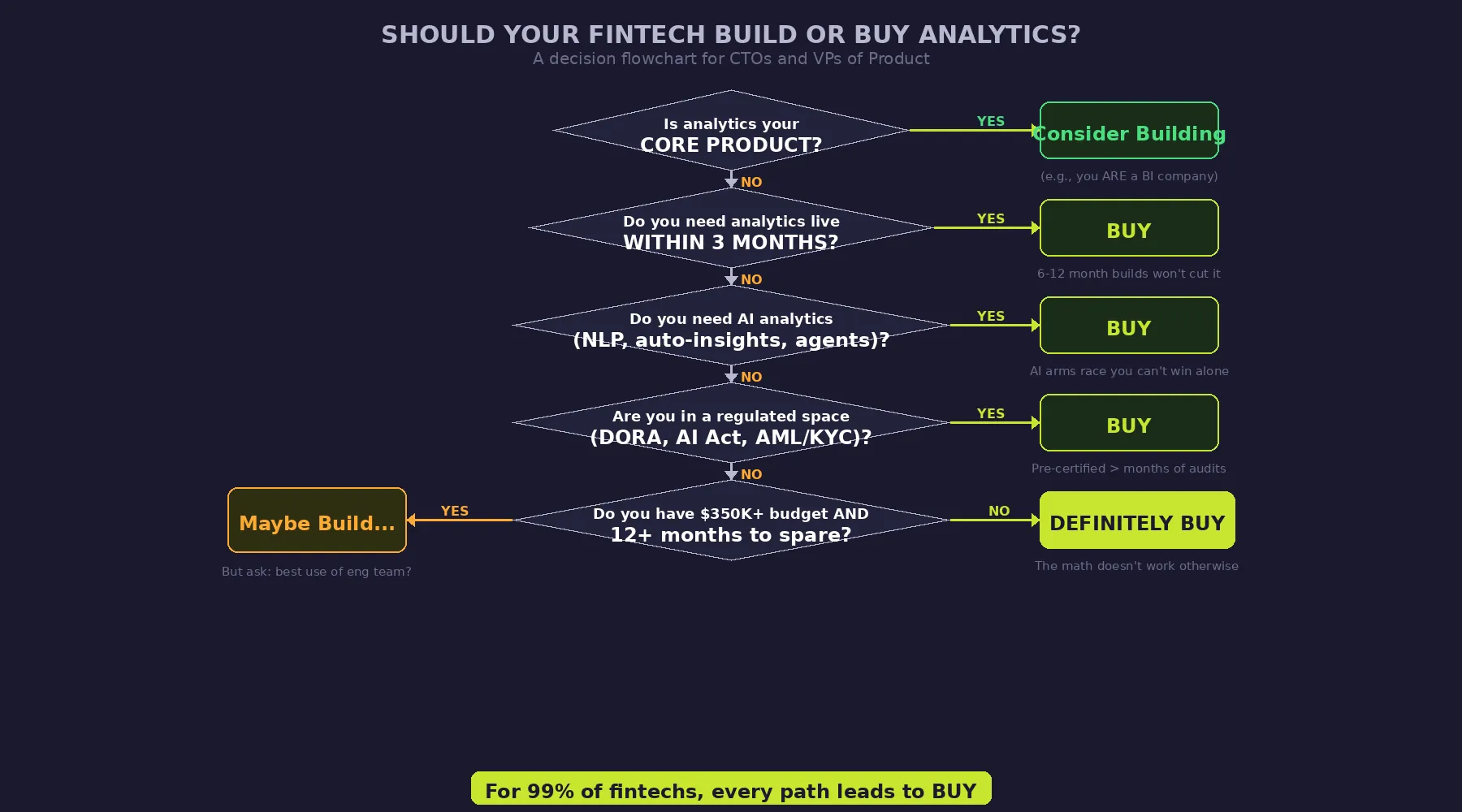

Why “Buy” Wins for Fintech in 2026

The build argument has exactly one strong case: when analytics IS your core product. If you’re a BI company, build. If you’re a fintech company that happens to need analytics — and that’s virtually all of them — the math points overwhelmingly toward buying.

Here’s why, and why the case is even stronger in 2026 than it was a year ago.

The AI Gap Is Accelerating

By 2026, more than 80% of software vendors will have generative AI embedded in their products. The analytics platforms you’d be competing against have dedicated teams building conversational analytics, auto-generated visualizations, and agentic BI capabilities. Building your own means you’re not just coding dashboards — you’re entering an AI arms race against companies whose entire business is analytics.

Luzmo’s recently launched Agent APIs illustrate this gap. They offer modular, AI-driven endpoints for dataset discovery, formula generation, natural language interaction, and automated visualization creation. Replicating this in-house would require ML engineers, NLP specialists, and ongoing model maintenance — a team and budget most fintechs can’t justify for a supporting feature.

Regulatory Deadlines Won’t Wait for Your Build Cycle

DORA enforcement is scaling in Q1 2026. MiCA’s transitional period ends mid-year. The EU AI Act’s high-risk system obligations take effect in August 2026, requiring financial institutions to map, audit, and remediate all AI deployments with strict transparency requirements.

If your analytics build cycle is 6–12 months, you’re starting now to maybe have something by the time these deadlines hit. A pre-certified embedded platform gives you compliant analytics in weeks, not quarters.

The Scalability Tax Is Real

Multi-tenant analytics with proper data isolation, SSO integration, role-based access, and audit trails is what Amazon would call “undifferentiated heavy lifting.” It’s essential, it’s complex, and it adds zero competitive advantage to your product.

One embedded analytics vendor reported that a leading information services company achieved 7x cost savings compared to what they would have spent building in-house. Zendesk found that after embedding an analytics solution, 80% of their Plus and Enterprise customers used dashboards daily — making analytics the primary driver of plan upgrades.

The pattern is clear: companies that treat analytics as infrastructure (buy it) outperform those that treat it as a build project.

The Luzmo Advantage for Fintech

If you’re going to buy, the platform needs to meet fintech-grade requirements. Here’s how Luzmo maps to the specific needs outlined in this article.

Speed: Weeks, Not Months

Luzmo’s drag-and-drop dashboard builder and API-first architecture mean your team can go from zero to production dashboards in two to six weeks. Native SDK components for React, Vue, and Angular ensure a smooth handoff from design to deployment. Your designers maintain full creative control — every pixel is customizable to match your brand.

AI-Powered Analytics (Agent APIs)

Luzmo IQ brings conversational analytics directly into your product. Users ask questions in natural language and get instant visual answers. The Agent API suite includes automated dataset descriptions, AI formula creation, natural language data discovery, and conversational query generation. The modular design lets you start with one agent and scale toward fully agentic analytics experiences without overhauling your stack.

Fintech-Ready Compliance

SOC-II and GDPR compliance comes pre-built. Multi-tenant architecture with native row-level security ensures proper data isolation for regulated fintech environments. SSO integration, audit trails, and access control layers are all included — not engineering projects.

Performance at Scale

The Warp query engine delivers sub-second dashboard loads, even with large financial datasets. Multi-currency and multi-timezone support is native, not bolted on. White-label branding means your analytics look like your product — not a third-party tool your customers need to learn.

Proven in Production

Companies using Luzmo have seen measurable results: Kenjo embedded production-ready analytics in weeks with minimal engineering effort. Spaceflow reduced analytics-related support requests by 80%. Fleet Perfection accelerated vehicle sales by 30% through better data visibility. These aren’t hypothetical projections — they’re production metrics from real deployments.

The Math Is Clear. Now Calculate Yours.

Here’s the decision in its simplest form:

You can spend $350K+ and 6–12 months building analytics that will be outdated by the time it ships. Or you can invest a fraction of that, launch in weeks, and get AI-powered, compliance-ready analytics that keeps pace with a rapidly evolving regulatory and competitive landscape.

Every month your team spends building chart components is a month your competitors are shipping AI-driven dashboards, winning enterprise deals with embedded compliance reporting, and reducing churn with self-service analytics their customers actually use.

The 2026 fintech market won’t wait for your build cycle. Your customers won’t either.

What to Do Next

Calculate your specific cost. Take your engineering team’s loaded hourly rate, multiply by the estimated build hours for multi-tenant analytics with compliance requirements, and compare it to a platform investment of $12–18K per year. Include the opportunity cost of delayed core product features. For most fintechs, the gap is 10–20x.

See it in action. Luzmo offers a free 10-day trial with no credit card required. Or talk to their product team for a guided demo focused on your specific fintech use case — whether that’s fraud analytics, lending dashboards, compliance reporting, or payments visibility.

The companies that get this right treat analytics as product infrastructure, not a side project. In 2026, that distinction is the difference between leading your market and chasing it.

Written by

Ship the future of your data

Let us show you what Luzmo can do for your product.

Leave your e-mail and one of our analytics experts will reach out to you