ChatGPT

ChatGPT

Perplexity

Perplexity

.png)

.png)

.png)

Build your first embedded data product now. Talk to our product experts for a guided demo or get your hands dirty with a free 10-day trial.

.png)

When FVCbank eliminated 60 hours of monthly manual reporting and reduced past-due loans by 75%, they didn't hire more analysts. They embedded analytics directly into their banking platform. When JPMorgan Chase saved $1.5 billion through fraud prevention and personalized services, the foundation was real-time, embedded analytics making 55 million decisions daily.

The BankTech sector has a hidden infrastructure crisis. As embedded finance explodes from $83 billion (2023) to a projected $370 billion by 2035, banks and fintechs are discovering that their analytics capabilities—or lack thereof—determine whether they capture this growth or get left behind.

This isn't about making prettier dashboards. It's about whether your platform can deliver the real-time insights that customers now expect, the compliance visibility that regulators demand, and the operational intelligence that separates profitable partnerships from money-losing ones.

Ninety-six percent of sponsor banks maintain 5+ fintech partnerships simultaneously. Each partnership generates mountains of data—transaction patterns, risk indicators, customer behavior, compliance signals. Without embedded analytics, this data becomes a liability instead of an asset.

The revenue stakes are clear: sponsor banks now earn 51.3% of their revenue from embedded finance partnerships. These aren't traditional banking relationships. They're API-driven, real-time, multi-tenant operations that generate insights measured in milliseconds, not monthly reports.

Consider the customer experience battleground:

.png)

You can't deliver personalization without analytics. You can't provide real-time insights with monthly batch reporting. And you certainly can't scale embedded finance partnerships while your team spends 60 hours a month manually creating reports in Excel.

Traditional BI tools were built for internal analysts, not customer-facing applications. When you try to embed Tableau or Power BI into your banking platform, you're forcing a square peg into a round hole. The result? 6-12 month implementation timelines, clunky iframe-based integrations that break your UX, and dashboards that load so slowly your customers give up.

Luzmo was built specifically for embedding analytics into SaaS platforms. The difference shows:

When a fintech needs to add analytics to their embedded lending product, they don't have time for a year-long implementation. With Luzmo, they can connect to their data warehouse, customize dashboards to match their brand, and ship analytics to customers in weeks.

BankTech platforms serve multiple customers, each with their own data that must remain completely isolated. A community bank offering Banking-as-a-Service to 10 fintech partners needs absolute certainty that Partner A can never see Partner B's data—not through a misconfiguration, not through a URL manipulation, not ever.

This is where generic BI tools fall apart. They weren't designed for multi-tenant SaaS architectures. You end up building complex middleware layers, managing separate database instances, or worse—trusting that your developers never make a security mistake.

Luzmo's multi-tenancy is built into the platform:

This matters enormously in banking. When 80% of sponsor banks face compliance challenges in their embedded finance programs, and 20% cite reputational damage as the biggest risk, security isn't optional—it's the foundation.

Banks and fintechs have spent years building brand trust. When customers open the analytics section of your app, they should see your brand, your design system, your user experience—not a dashboard that screams "this is a third-party BI tool."

Traditional BI platforms offer limited customization. Sure, you can change the logo and maybe adjust some colors. But the underlying UI patterns, interaction models, and visual language remain distinctly "not yours." Users notice. Product teams notice. Executives definitely notice.

Luzmo enables true white-labeling:

When a digital bank embeds analytics into their mobile app, customers should have no idea they're looking at Luzmo-powered dashboards. They should just experience beautifully integrated analytics that feel native to the app they already know.

Here's the BankTech paradox: customers demand self-service analytics, but most platforms can't deliver it without creating an unsustainable support burden.

Give users a full BI tool and they're overwhelmed—tickets flood in about how to create calculations, join datasets, or build specific visualizations. Lock down the analytics too much and users complain they can't get the insights they need, leading to endless feature requests for "just one more dashboard."

Luzmo solves this through tiered self-service:

For less technical users:

For power users:

For developers:

This flexibility is critical in Banking-as-a-Service models. A platform serving both small businesses and enterprise clients needs analytics that scale across skill levels—simple for beginners, powerful for experts, and never requiring a support ticket to accomplish common tasks.

.png)

The measurable impact of proper embedded analytics in BankTech:

Operational efficiency:

Revenue growth:

Customer experience:

Compliance & risk:

Banking analytics isn't generic BI. The requirements are specific and unforgiving:

Real-time or nothing: Monthly reports were fine in 2010. In 2026, banks monitor liquidity minute-by-minute, detect fraud in milliseconds, and personalize offers in real-time. Batch processing doesn't cut it.

Compliance-first architecture: Every query needs an audit trail. Every user action must be logged. Data residency matters. GDPR compliance isn't optional. The platform needs SOC 2 certification. Generic BI tools treat these as afterthoughts; in banking, they're prerequisites.

Performance at scale: A fintech processing 1M transactions daily generates massive datasets. Analytics queries can easily span hundreds of millions of rows. If your embedded analytics platform takes 20 seconds to load a dashboard, you've already lost the user.

Luzmo addresses these requirements through:

BankTech platforms are built on modern data infrastructure: Snowflake, BigQuery, Redshift, Databricks. Your analytics platform needs to work natively with these tools, not force you to duplicate data into yet another database.

Luzmo connects directly to:

The integration is straightforward:

This "work with your existing stack" philosophy matters enormously. BankTech teams don't want another database to manage, another ETL pipeline to maintain, or another data synchronization process to monitor. They want analytics that plug into what they've already built.

According to American Banker's 2025 survey of 212 banking executives, the top IT investment priorities are:

.png)

Notice that data analytics ranks #2, right behind security—and effective analytics enhances security by enabling real-time fraud detection and risk monitoring.

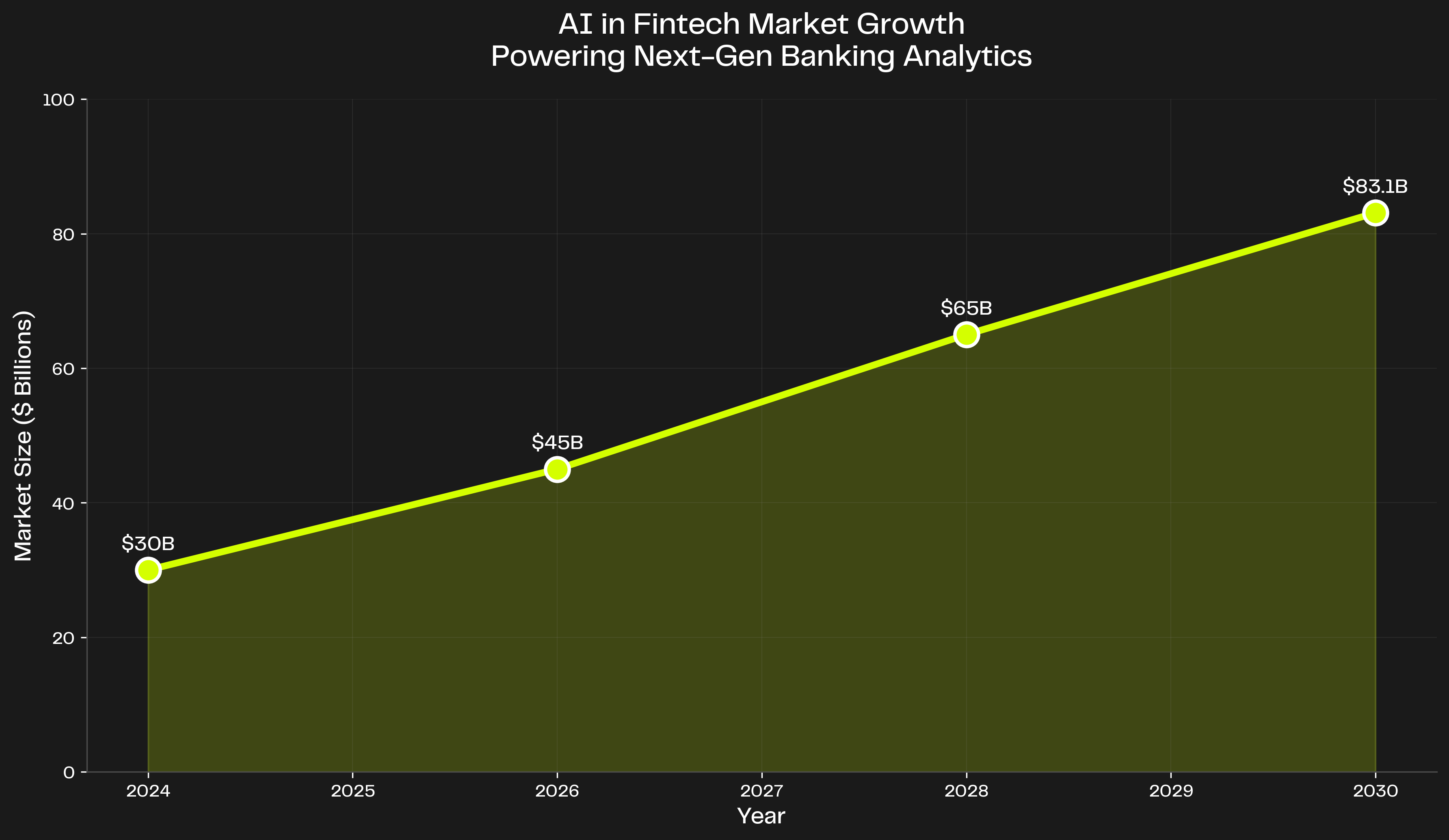

The AI in fintech market is growing from $30B (2025) to $83.1B (2030). This growth is driven by embedded analytics platforms that make AI insights accessible to end users, not just data scientists.

Five years ago, you could argue for building analytics in-house. In 2026, that argument is harder to make:

Why building in-house fails:

Why buying Luzmo works:

The "build" option made sense when no good embedded analytics platforms existed. Today, with mature solutions designed specifically for your use case, building is expensive vanity.

Your competitors are embedding analytics. The question isn't "should we?" but "how fast can we ship?"

When 94% of financial institutions plan to invest in compliance technologies leveraging analytics, and 80% of fintech investors prioritize AI-based solutions, the market has spoken: analytics infrastructure is no longer optional.

Consider the competitive dynamics:

Without embedded analytics:

With embedded analytics:

The strategic advantage is clear. Analytics isn't a feature—it's the foundation that makes everything else possible.

If you're building or scaling a BankTech platform in 2026, embedded analytics should be in your roadmap for Q1. Here's why:

For digital banks: Your customers expect spending insights, budget tracking, and financial health scores embedded directly in your app. These aren't "nice to have" features—they're baseline expectations. 65% of U.S. adults expect to accomplish any financial task through a mobile app, and "any task" includes understanding where their money goes.

For Banking-as-a-Service platforms: Your fintech partners need dashboards showing transaction volumes, approval rates, revenue, and customer behavior. They need white-label analytics they can offer their customers. You need visibility into partner performance. None of this works with quarterly PDF reports.

For embedded lending products: Credit decisions require real-time risk assessment. Merchants need instant visibility into approval rates, average ticket sizes, and transaction patterns. Buy-now-pay-later providers need analytics showing conversion rates, default rates, and customer lifetime value. Speed matters—and spreadsheets don't cut it.

For payment processors: Merchants want to see transaction volumes, settlement timelines, chargeback rates, and fee calculations in real-time. Enterprise clients need analytics they can share with their finance teams. Self-service analytics reduce your support burden while increasing customer satisfaction.

Embedded finance is growing to $370 billion by 2035. AI in fintech is growing to $83 billion by 2030. Sponsor banks are earning 51% of revenue from partnerships. All of this growth depends on analytics infrastructure that can deliver real-time insights, maintain security, scale across customers, and empower users without creating support nightmares.

Luzmo was built specifically to solve these challenges. Not as a generic BI tool that happens to embed, but as a purpose-built embedded analytics platform designed for the exact requirements of SaaS platforms serving the financial sector.

The institutions winning in BankTech aren't building analytics from scratch. They're shipping customer-facing insights in weeks, not months. They're offering white-label analytics to partners. They're reducing support burden through self-service. They're meeting compliance requirements without custom engineering.

Your competitors are already doing this. The question is: how long will you wait?

Ready to see how embedded analytics can accelerate your BankTech platform?

Book a demo with Luzmo to see how you can ship analytics in weeks, not months—with the security, performance, and flexibility that banking requires.

All your questions answered.

Build your first embedded data product now. Talk to our product experts for a guided demo or get your hands dirty with a free 10-day trial.